The next strategic frontiers of medtech

Where should medtech and femtech companies focus their international expansion efforts after establishing EU and US market presence? This article analyses eight high-potential markets across four global regions — Anglosphere, East Asia, MENA, and Latin America — ranked against three strategic criteria: ROI and medtech infrastructure, femtech readiness, and regulatory alignment with international harmonisation frameworks including MDSAP and CE Mark mutual recognition agreements. Whether you are mapping your next regulatory strategy or building a market entry roadmap, this evidence-based analysis offers a practical starting point — with an honest look at what the data says and where gut instinct still has a role to play.

After my popular recent poll, which strategic markets deserve to be your and my next medtech focus beyond US-EU? Note: beyond, not instead of!

What are the factors we want to optimise?

ROI & MEDTECH INFRASTRUCTURE: markets that offer the highest investment and monetization potential, with advanced payer structures and tech scaling capabilities.

FEMTECH READINESS: regions where the cultural and policy discourse is opening to women’s health, where clinical research is advanced, and femtech innovation and startup ecosystem are thriving.

REGULATORY ALIGNMENT: countries that align with international medtech harmonisation efforts, for example being members of MDSAP or with mutual recognition agreements (MRA) towards CE mark and FDA.

With the help of Claude, I ran an advanced analysis to find the right countries for these categories. More details on the results summarised below.

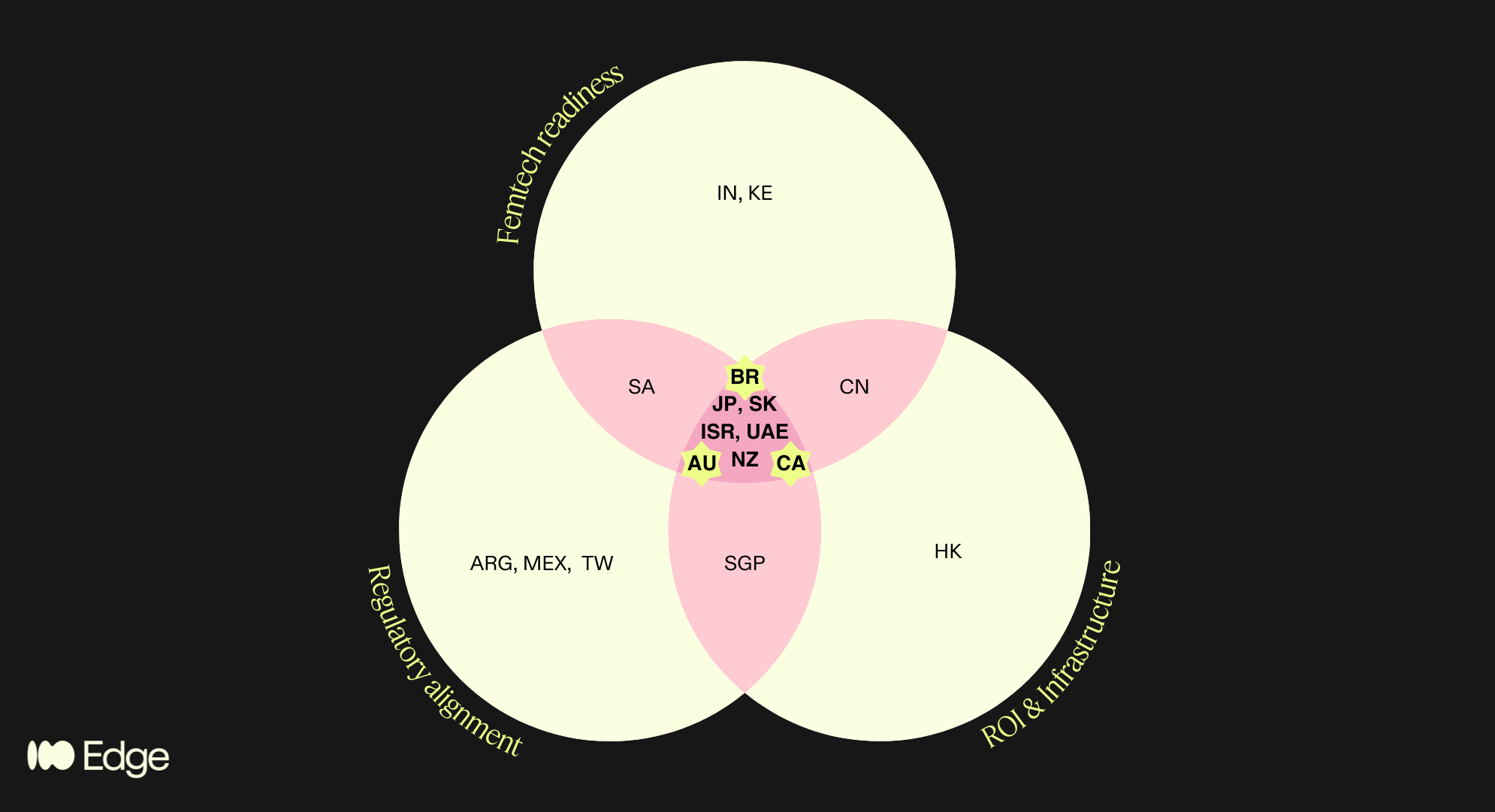

Regions that satisfied multiple criteria are highlighted in the pink areas of the diagram. This brings us to 8 high potential regions, spanning the 4 geographies of my poll!

Anglosphere: Canada, Australia, New Zealand

“BRIC”+East Asia: Japan, South Korea

MENA: Israel, UAE

LatAm: Brazil

What does it mean for your market strategy? If you are in femtech and looking to expand after EU/US proof-of-concept - AND not planning to exit directly - then these are your markets. Save and share the post, and narrow down the list based on further criteria relevant to you and your business.

To me and my business, I applied the following additional criteria:

Accessibility: where can my cultural roots and the languages I speak help me?

Market size: >20M for highest chances of leads and indirect product reach for my clients

Heterogeneity: the more diverse the better for clinical research relevance

Geopolitical stability: low risk of conflicts and market volatility

Which takes us to the winners!

🇧🇷 Brasil: as half-Brazilian I’ll be proud and excited to explore the femtech, clinical and regulatory space and build connections there! DM me to discuss!

🇦🇺 🇨🇦 Australia and Canada: it’s a tie! I already work with these markets, no big lift, but good pointer to go a bit deeper. Spoiler: more MDSAP content coming, like it or not..!

🇦🇪 UAE: Although it didn’t pass my filters, something in my gut tells me not to give up on it. I’d love to partner up with medtech experts and providers in that area.

This aligns well with the results from the poll: 52 votes, indicating predominant interest in "anglosphere" (32%) and "emerging" (30%), incl. LatAm.

Thanks to all who voted, commented and even called me to share their passionate insights!

Deep dive

The framework: three lenses, not one

We structured the analysis around three criteria, chosen because they reflect the real bottlenecks that founders face when entering new markets.

Regulatory alignment (MDSAP / MRAs). For a CE-marked or FDA-cleared device, the most efficient path into a new market is one that recognises or aligns with those approvals. The Medical Device Single Audit Program (MDSAP) is the primary international harmonisation vehicle, currently comprising the US (FDA), Canada (Health Canada), Brazil (ANVISA), Australia (TGA), and Japan (PMDA). Beyond MDSAP, a growing network of Mutual Recognition Agreements (MRAs) extends this regulatory compatibility further — most notably, the EU–Australia MRA, Israel's deep alignment with EU MDR, South Korea's MFDS harmonisation pathway, and GCC's increasing adoption of CE and FDA as reference standards.

Femtech readiness. This goes beyond market size. It asks whether the cultural, policy, and clinical infrastructure of a market is genuinely open to women's health innovation — or whether femtech companies will spend the first two years of market entry fighting the problem rather than solving it. We looked at startup density, clinical research activity, regulatory openness to digital health, and the status of women's health policy discourse in each candidate country.

ROI and medtech infrastructure. Commercial viability ultimately depends on whether a market can pay for solutions and scale them. This means evaluating healthcare financing structures (private payer vs. public reimbursement vs. out-of-pocket), digital health infrastructure, startup ecosystem depth, and the presence of credible distribution and partnership networks.

Only markets that scored meaningfully across all three lenses made the final shortlist. That intersection — regulatory alignment AND femtech readiness AND commercial infrastructure — is the filter that separated 8 markets from the 25+ we considered.

The 25-country universe and how it narrowed

We mapped approximately 25 countries across the three criteria, drawing on data from:

Institute for Economics & Peace Global Peace Index 2024 (163 countries) for geopolitical stability scoring

EF English Proficiency Index 2024 (116 countries) for accessibility

UN Population data 2024 for market size

World Bank ethnic fractionalization data for demographic heterogeneity (relevant to clinical research representativeness)

Vestbee, Dealroom, Speedinvest, Grand View Research, Startups Magazine for femtech market data by country

MDSAP member country documentation and publicly available MRA registers for regulatory alignment

Countries in only one or two circles of the Venn include genuinely interesting markets — Singapore (strong MDSAP alignment and infrastructure but too small for standalone commercial focus), India (exceptional femtech growth projected at 17.8% CAGR to 2030 per Grand View Research, but regulatory alignment is a work in progress), South Africa (emerging femtech ecosystem with strong policy momentum, but infrastructure gaps and geopolitical risk), China (significant commercial potential but regulatory and geopolitical friction makes it a poor fit for EU-anchored companies), and Kenya (one of Africa's most active femtech ecosystems, but not yet operationally viable for most European companies without a dedicated local strategy).

These are not dismissed markets — they are markets for a different risk appetite or a later stage.

The 8 that made the intersection

These are the markets that sat inside all three criteria simultaneously. For each, we break down the case across the three categories.

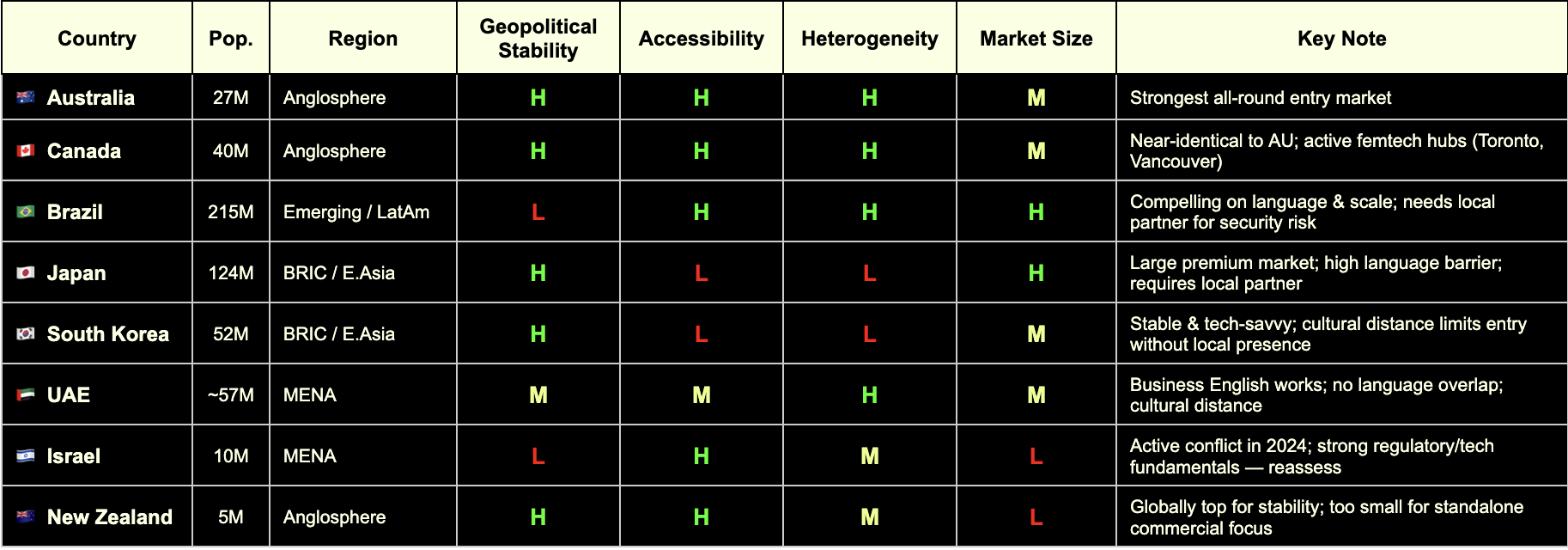

🇦🇺 Australia

Regulatory Alignment

MDSAP full member (TGA)

EU–Australia Mutual Recognition Agreement in place — CE mark directly supports TGA approval pathway

Strong alignment with ISO 13485 and IEC 62304 for software-based devices

Femtech Readiness

Mature digital health market with active government investment (Australian Digital Health Agency)

Women's health policy discourse is open and progressive; no significant cultural friction for femtech categories

Active medtech and healthtech startup ecosystem, particularly in Melbourne and Sydney

ROI & Infrastructure

Population ~27 million; 27% foreign-born (one of OECD's highest) — valuable for diverse clinical evidence

Mixed public/private payer system; growing private digital health reimbursement

English-speaking, Commonwealth-aligned, low operational complexity

GPI 2024: #17 — high geopolitical stability

🇨🇦 Canada

Regulatory Alignment

MDSAP founding member (Health Canada)

A single MDSAP audit covers Canada alongside the US, Brazil, Australia, and Japan — significant efficiency gain

Health Canada increasingly aligned with FDA on digital health device classification

Femtech Readiness

Toronto and Vancouver are active femtech hubs; Femtech Canada is an established national ecosystem

Strong clinical research infrastructure with diverse patient populations

Progressive women's health policy environment; high awareness and destigmatisation of femtech categories

ROI & Infrastructure

Population ~40 million; ~27% immigrant share — comparable diversity to Australia

Robust private and public payer landscape; provincial variation requires navigation

English and French markets; English operations are broadly sufficient for market entry

GPI 2024: #13 — highly stable

🇧🇷 Brazil

Regulatory Alignment

MDSAP full member via ANVISA — the most underutilised structural advantage for European companies entering LatAm

A single quality audit unlocks market access across all five MDSAP jurisdictions simultaneously

ANVISA has been modernising its device framework; registration timelines have improved significantly

Femtech Readiness

Growing digital health and femtech ecosystem, particularly in São Paulo and Rio de Janeiro

Large, young, highly digitally engaged female population

Significant unmet need in reproductive health, maternal health, and menstrual care — high receptivity to femtech solutions

ROI & Infrastructure

Population ~215 million — the largest in Latin America by a substantial margin

Highest ethnic fractionalization score globally (World Bank) — clinical data generated here is maximally representative

⚠️ GPI 2024: #131 — operational complexity is real; security considerations, contract risk, and local partner dependency must be factored in

Local partner infrastructure is a prerequisite, not an option

🇯🇵 Japan

Regulatory Alignment

MDSAP full member via PMDA (Pharmaceuticals and Medical Devices Agency)

PMDA is one of the most rigorous regulatory bodies globally; MDSAP audit significantly reduces duplicative burden

Regulatory pathway for digital health devices (SaMD) is well-defined

Femtech Readiness

One of the world's most advanced femtech markets by per-capita spend on menstrual health and reproductive technology

Strong clinical research infrastructure and data quality

⚠️ Cultural norms around women's health are evolving but remain conservative in some categories — market education investment required

ROI & Infrastructure

Population ~124 million; high healthcare spending and premium consumer health culture

High-margin market for validated, evidence-backed products

⚠️ EF English Proficiency Index: #92 out of 116 — significant language barrier; local partner or Japanese-speaking regulatory lead is non-negotiable

GPI 2024: #11 — very high stability

🇰🇷 South Korea

Regulatory Alignment

MFDS (Ministry of Food and Drug Safety) has progressively aligned with FDA and EU MDR frameworks

MDSAP compatibility pathway is expanding; not yet full membership but convergence is directional

Government actively promoting K-healthcare internationally — creating reciprocal openings for foreign market entry

Femtech Readiness

High digital health adoption and smartphone penetration; strong consumer appetite for health tracking and wearables

Growing awareness of women's health, particularly in fertility and menstrual health tech

Active startup ecosystem with increasing women's health focus

ROI & Infrastructure

Population ~52 million; advanced payer structures and tech scaling infrastructure

Government investment in digital health innovation is substantial

⚠️ EF EPI: #50 — business English limited outside Seoul; local presence required

GPI 2024: #46 — stable, with standard geopolitical considerations given peninsula context

🇮🇱 Israel

Regulatory Alignment

Israeli MOH operates with strong alignment to EU MDR and FDA standards — one of the most harmonised non-MDSAP markets globally

CE mark is a recognised reference standard; dual EU/FDA submission strategies are well-established

Deep bilateral ties with both EU and US regulatory bodies

Femtech Readiness

Exceptionally strong clinical research infrastructure; Israel produces a disproportionate number of medtech innovations relative to population

Highly developed VC and medtech ecosystem; femtech companies including HeraMed are globally recognised

High awareness and openness to women's health innovation; destigmatisation is advanced relative to regional peers

ROI & Infrastructure

Population ~10 million — small absolute market, but high income and high health spend per capita

English proficiency high (EF EPI: #51); business environment is highly accessible to European operators

Strong potential as a clinical trial site and R&D partnership hub, regardless of commercial scale

⚠️ GPI 2024: #155 — reflects active conflict situation as of the 2024 index; market entry decisions require live geopolitical risk assessment, not a static one. The underlying regulatory, clinical, and commercial infrastructure remains among the strongest in this cohort

🇦🇪 GCC (UAE & Saudi Arabia)

Regulatory Alignment

Neither is a formal MDSAP member, but UAE and KSA have adopted CE mark and FDA clearance as primary reference pathways for device registration

UAE MOHAP and Saudi SFDA increasingly streamlined; CE mark provides a strong starting point

GCC Standardization Organization (GSO) harmonisation creates some regional regulatory efficiency

Femtech Readiness

Saudi Arabia's Vision 2030 explicitly references women's empowerment and healthcare improvement — femtech is policy-aligned

UAE has the most open and internationally diverse women's health market in the region

Growing investor interest in femtech and digital health across the Gulf; GITEX Health and Arab Health are active deal-making forums

ROI & Infrastructure

UAE: ~89% of resident population is expatriate (UN data) — genuinely diverse patient population and cosmopolitan business environment

English is the functional operating language for business in both markets

Premium private-pay market; reimbursement structures favour high-value, evidence-backed products

⚠️ GPI 2024: UAE #53 (improved 31 places in 2024 — single largest improvement in the index); KSA requires ongoing monitoring

Cultural distance to women's health topics exists in some categories — local partnership and community navigation are important

🇳🇿 New Zealand

Regulatory Alignment

MDSAP full member (Medsafe)

Strong regulatory alignment with Australia (TGA); joint Trans-Tasman regulatory considerations apply

Simple, transparent regulatory environment — among the most accessible globally for device registration

Femtech Readiness

Progressive women's health policy environment; high health literacy and digital engagement

Maori and Pacific women's health is an active policy and research priority — relevant for inclusive femtech design and clinical evidence

English-speaking, low cultural friction across all standard femtech categories

ROI & Infrastructure

Population ~5 million — too small for standalone commercial focus

Best positioned as a clinical trial jurisdiction, regulatory proof-of-concept market, or Australasian stepping stone alongside Australia

GPI 2024: #4 — among the most geopolitically stable countries on earth

High income per capita; public system (Pharmac) for reimbursement is conservative but private market is accessible

What this means for women’s health startups

The eight markets are not interchangeable, and we are not suggesting a company should pursue all of them simultaneously. The practical read is this:

For a femtech company at the EU/US proof-of-concept stage, with limited expansion resources and no existing presence outside Europe, Australia and Canada are the lowest-friction first moves. They are MDSAP members, English-speaking, culturally accessible, and have enough market depth to justify the investment.

Brazil becomes compelling the moment you have a local partner or are prepared to build one. The MDSAP pathway is a structural advantage that is consistently underutilised by European companies, and a population of 215 million — with the highest demographic diversity of any market on this list — is a significant clinical research and commercial prize.

Japan and South Korea are high-reward markets that require deliberate localisation investment. The regulatory frameworks are accessible through MDSAP and MRA alignment; the human infrastructure needs to be built.

Israel and the GCC are specialist considerations — Israel for companies with strong clinical trial and research ambitions, the GCC for companies targeting the premium private-pay women's health segment and building into the Middle East and North Africa corridor.

New Zealand is genuinely valuable as a regulatory and clinical site — less so as a primary commercial target.

The 4th lens…

At Edge Compliance we want to keep serving US and EU market entries (EU as a continent, incl. UK and CH).

What this analysis taught us is where to put our next focus in terms of partnerships, network, learning, advocacy.

In order to avoid spreading ourselves too thinly, we applied some filters to narrow down the list of high potential regions to a smaller selection. The Edge Compliance lens considers:

Cultural accessibility

Market size

Demographic heterogeneity

Geopolitical stability

Criteria for market selection for Edge Compliance. Which are relevant to your business?

This analysis led us to choose the following areas of focus in addition to our existing focus and expertise:

🇧🇷 Brasil

🇦🇺 Australia

🇨🇦 Canada

🇦🇪 UAE

We trust this will help us help YOU with future-proof regulatory strategy and foresight that is ahead of trends.

References

Institute for Economics & Peace GPI 2024

EF English Proficiency Index 2024

UN World Population Prospects 2024

World Bank Ethnic Fractionalization Data

Vestbee Femtech Market Overview (2024)

Dealroom Femtech Report (2024)

Speedinvest Femtech Investment Analysis

Grand View Research India Femtech Market Outlook 2024–2030

MD+DI FemTech Analytics (2024)

Startups Magazine Southeast Asia Femtech Report

The Recursive CEE Femtech Analysis (2025)

Methodology note: This Deep Dive is based on my original LinkedIn post, reflecting my professional experiences and personal perspectives. Claude AI assisted in elaborating the topic into a broader article by integrating personal notes, literature research, fact-checking and deeper insights on the topic. All analysis and regulatory perspectives are my own, and all content has been reviewed by me for accuracy.

PCCP beyond AI

Very exciting trend of femtech apps integrating with wearable data! How does this work for the regulated ones? I wanted to share this clever use of PCCP from Natural Cycles° from last year which impressed me.

What's PCCP?

Pre-determined Change Control Plan is a regulatory instrument devised by FDA - as a European is I'm most jealous of. It was designed to enable AI devices, which by design need to be able to evolve their accuracy in the field, getting smarter the more data they acquire. Traditionally, any change to the accuracy and performance of a device required a regulatory resubmission (still the case in EU) and up to 90 days of review wait.

With PCCP you can get pre-approval for a reasonable range of performance that you anticipate and accept.

What I found clever, is that Natural Cycles°, the pioneer of regulated fertility awareness, used PCCP not for AI changes but for variability of source data from different wearables.

While, as far as I'm aware, they currently integrate only with ŌURA and Apple Watch, this clears the way for them to swiftly add any more integrations to their conception/contraception suite as long as they fit their predefined specs (see table in pdf).

This is an example of how:

1️⃣ Regulatory instruments that are smart and abreast with the times enable even more innovation than what they primarily intended to,

2️⃣ Femtech is riding the wave of biomarkers ensuring most users can be served irrespective of which devices they choose - it's not just the iOS vs Android divide anymore!

3️⃣ Scientific research and clinical partnerships will see an incredible boost of opportunity from all this data, finally compensating for the lack of data that we know womens health has suffered until now!

What else could we use PCCP for? And until when can we have a similar toolkit in Europe under MDR? 🫠

NC's current integrations here

Link to full 510k summary here

At Women’s Health Week Europe

The go-to regulatory compliance agency for femtech. Find out more.

An absolutely incredible time at Women's Health Week at the Barbican! The opportunity and momentum for femtech re undeniable.

It's no philanthropic initiative, it's a business sector with real problems be solved and real money to be made. Women, i.e. 51% of the population, control more than 80% of household health decisions, yet suffer ill-health for 19% more time than men - mostly during their working years.

Closing the gap could generate >$1trillion annual global GDP by 2040. It's no charity, it's business sense.

The innovation that is happening in this space fills us with awe, anticipation and gratitude. Will post more about some of the founders and products that we learnt about.