The next strategic frontiers of medtech

Where should medtech and femtech companies focus their international expansion efforts after establishing EU and US market presence? This article analyses eight high-potential markets across four global regions — Anglosphere, East Asia, MENA, and Latin America — ranked against three strategic criteria: ROI and medtech infrastructure, femtech readiness, and regulatory alignment with international harmonisation frameworks including MDSAP and CE Mark mutual recognition agreements. Whether you are mapping your next regulatory strategy or building a market entry roadmap, this evidence-based analysis offers a practical starting point — with an honest look at what the data says and where gut instinct still has a role to play.

After my popular recent poll, which strategic markets deserve to be your and my next medtech focus beyond US-EU? Note: beyond, not instead of!

What are the factors we want to optimise?

ROI & MEDTECH INFRASTRUCTURE: markets that offer the highest investment and monetization potential, with advanced payer structures and tech scaling capabilities.

FEMTECH READINESS: regions where the cultural and policy discourse is opening to women’s health, where clinical research is advanced, and femtech innovation and startup ecosystem are thriving.

REGULATORY ALIGNMENT: countries that align with international medtech harmonisation efforts, for example being members of MDSAP or with mutual recognition agreements (MRA) towards CE mark and FDA.

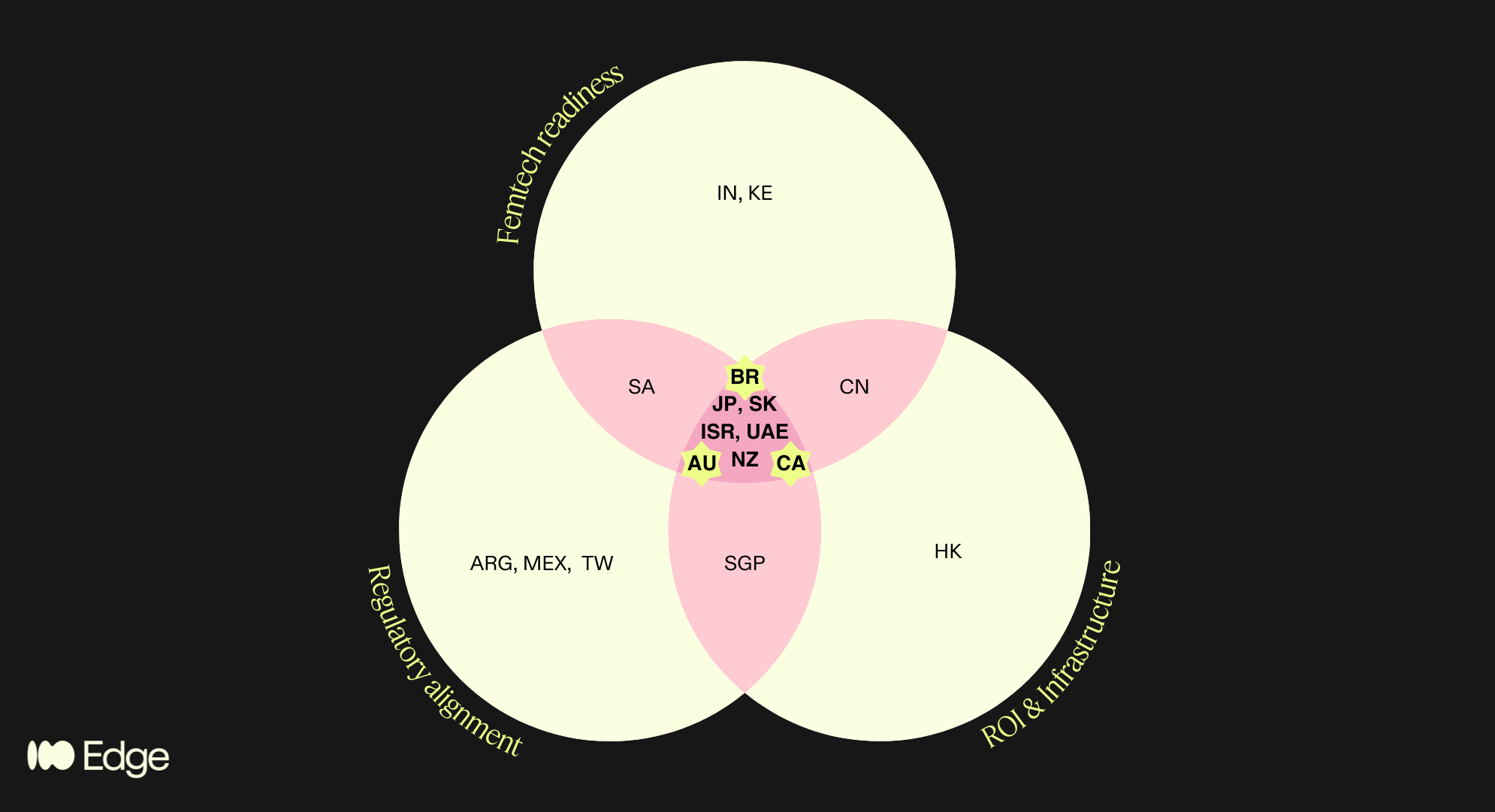

With the help of Claude, I ran an advanced analysis to find the right countries for these categories. More details on the results summarised below.

Regions that satisfied multiple criteria are highlighted in the pink areas of the diagram. This brings us to 8 high potential regions, spanning the 4 geographies of my poll!

Anglosphere: Canada, Australia, New Zealand

“BRIC”+East Asia: Japan, South Korea

MENA: Israel, UAE

LatAm: Brazil

What does it mean for your market strategy? If you are in femtech and looking to expand after EU/US proof-of-concept - AND not planning to exit directly - then these are your markets. Save and share the post, and narrow down the list based on further criteria relevant to you and your business.

To me and my business, I applied the following additional criteria:

Accessibility: where can my cultural roots and the languages I speak help me?

Market size: >20M for highest chances of leads and indirect product reach for my clients

Heterogeneity: the more diverse the better for clinical research relevance

Geopolitical stability: low risk of conflicts and market volatility

Which takes us to the winners!

🇧🇷 Brasil: as half-Brazilian I’ll be proud and excited to explore the femtech, clinical and regulatory space and build connections there! DM me to discuss!

🇦🇺 🇨🇦 Australia and Canada: it’s a tie! I already work with these markets, no big lift, but good pointer to go a bit deeper. Spoiler: more MDSAP content coming, like it or not..!

🇦🇪 UAE: Although it didn’t pass my filters, something in my gut tells me not to give up on it. I’d love to partner up with medtech experts and providers in that area.

This aligns well with the results from the poll: 52 votes, indicating predominant interest in "anglosphere" (32%) and "emerging" (30%), incl. LatAm.

Thanks to all who voted, commented and even called me to share their passionate insights!

Deep dive

The framework: three lenses, not one

We structured the analysis around three criteria, chosen because they reflect the real bottlenecks that founders face when entering new markets.

Regulatory alignment (MDSAP / MRAs). For a CE-marked or FDA-cleared device, the most efficient path into a new market is one that recognises or aligns with those approvals. The Medical Device Single Audit Program (MDSAP) is the primary international harmonisation vehicle, currently comprising the US (FDA), Canada (Health Canada), Brazil (ANVISA), Australia (TGA), and Japan (PMDA). Beyond MDSAP, a growing network of Mutual Recognition Agreements (MRAs) extends this regulatory compatibility further — most notably, the EU–Australia MRA, Israel's deep alignment with EU MDR, South Korea's MFDS harmonisation pathway, and GCC's increasing adoption of CE and FDA as reference standards.

Femtech readiness. This goes beyond market size. It asks whether the cultural, policy, and clinical infrastructure of a market is genuinely open to women's health innovation — or whether femtech companies will spend the first two years of market entry fighting the problem rather than solving it. We looked at startup density, clinical research activity, regulatory openness to digital health, and the status of women's health policy discourse in each candidate country.

ROI and medtech infrastructure. Commercial viability ultimately depends on whether a market can pay for solutions and scale them. This means evaluating healthcare financing structures (private payer vs. public reimbursement vs. out-of-pocket), digital health infrastructure, startup ecosystem depth, and the presence of credible distribution and partnership networks.

Only markets that scored meaningfully across all three lenses made the final shortlist. That intersection — regulatory alignment AND femtech readiness AND commercial infrastructure — is the filter that separated 8 markets from the 25+ we considered.

The 25-country universe and how it narrowed

We mapped approximately 25 countries across the three criteria, drawing on data from:

Institute for Economics & Peace Global Peace Index 2024 (163 countries) for geopolitical stability scoring

EF English Proficiency Index 2024 (116 countries) for accessibility

UN Population data 2024 for market size

World Bank ethnic fractionalization data for demographic heterogeneity (relevant to clinical research representativeness)

Vestbee, Dealroom, Speedinvest, Grand View Research, Startups Magazine for femtech market data by country

MDSAP member country documentation and publicly available MRA registers for regulatory alignment

Countries in only one or two circles of the Venn include genuinely interesting markets — Singapore (strong MDSAP alignment and infrastructure but too small for standalone commercial focus), India (exceptional femtech growth projected at 17.8% CAGR to 2030 per Grand View Research, but regulatory alignment is a work in progress), South Africa (emerging femtech ecosystem with strong policy momentum, but infrastructure gaps and geopolitical risk), China (significant commercial potential but regulatory and geopolitical friction makes it a poor fit for EU-anchored companies), and Kenya (one of Africa's most active femtech ecosystems, but not yet operationally viable for most European companies without a dedicated local strategy).

These are not dismissed markets — they are markets for a different risk appetite or a later stage.

The 8 that made the intersection

These are the markets that sat inside all three criteria simultaneously. For each, we break down the case across the three categories.

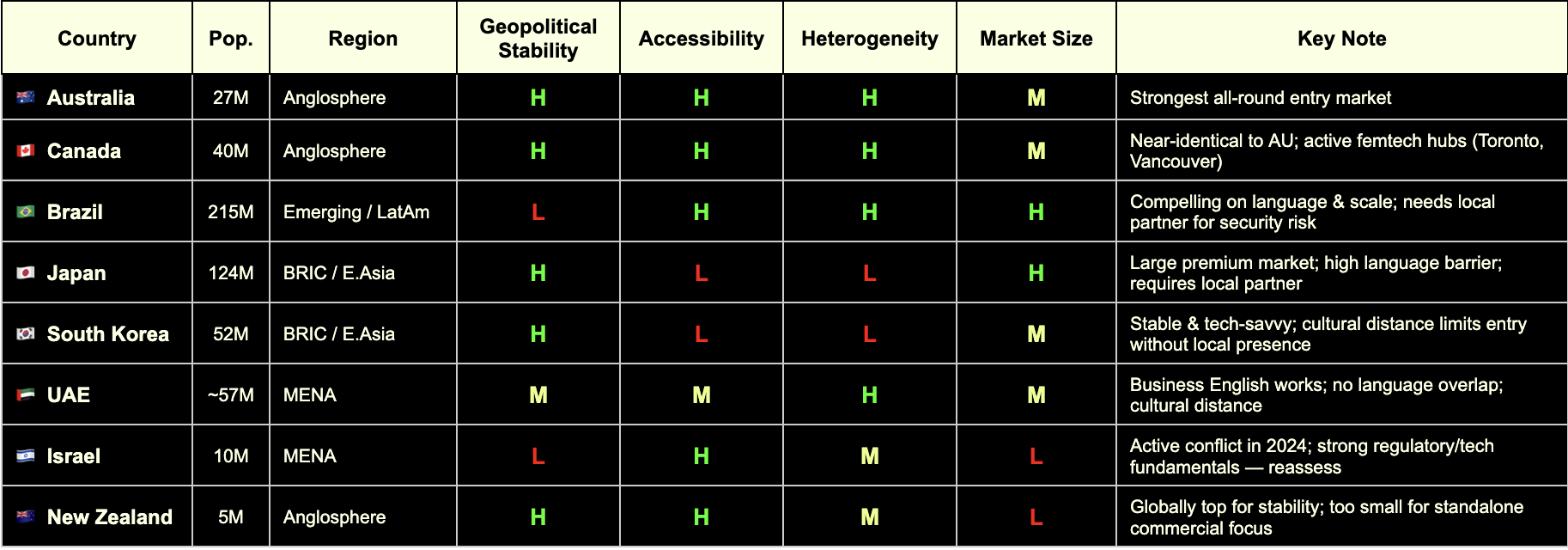

🇦🇺 Australia

Regulatory Alignment

MDSAP full member (TGA)

EU–Australia Mutual Recognition Agreement in place — CE mark directly supports TGA approval pathway

Strong alignment with ISO 13485 and IEC 62304 for software-based devices

Femtech Readiness

Mature digital health market with active government investment (Australian Digital Health Agency)

Women's health policy discourse is open and progressive; no significant cultural friction for femtech categories

Active medtech and healthtech startup ecosystem, particularly in Melbourne and Sydney

ROI & Infrastructure

Population ~27 million; 27% foreign-born (one of OECD's highest) — valuable for diverse clinical evidence

Mixed public/private payer system; growing private digital health reimbursement

English-speaking, Commonwealth-aligned, low operational complexity

GPI 2024: #17 — high geopolitical stability

🇨🇦 Canada

Regulatory Alignment

MDSAP founding member (Health Canada)

A single MDSAP audit covers Canada alongside the US, Brazil, Australia, and Japan — significant efficiency gain

Health Canada increasingly aligned with FDA on digital health device classification

Femtech Readiness

Toronto and Vancouver are active femtech hubs; Femtech Canada is an established national ecosystem

Strong clinical research infrastructure with diverse patient populations

Progressive women's health policy environment; high awareness and destigmatisation of femtech categories

ROI & Infrastructure

Population ~40 million; ~27% immigrant share — comparable diversity to Australia

Robust private and public payer landscape; provincial variation requires navigation

English and French markets; English operations are broadly sufficient for market entry

GPI 2024: #13 — highly stable

🇧🇷 Brazil

Regulatory Alignment

MDSAP full member via ANVISA — the most underutilised structural advantage for European companies entering LatAm

A single quality audit unlocks market access across all five MDSAP jurisdictions simultaneously

ANVISA has been modernising its device framework; registration timelines have improved significantly

Femtech Readiness

Growing digital health and femtech ecosystem, particularly in São Paulo and Rio de Janeiro

Large, young, highly digitally engaged female population

Significant unmet need in reproductive health, maternal health, and menstrual care — high receptivity to femtech solutions

ROI & Infrastructure

Population ~215 million — the largest in Latin America by a substantial margin

Highest ethnic fractionalization score globally (World Bank) — clinical data generated here is maximally representative

⚠️ GPI 2024: #131 — operational complexity is real; security considerations, contract risk, and local partner dependency must be factored in

Local partner infrastructure is a prerequisite, not an option

🇯🇵 Japan

Regulatory Alignment

MDSAP full member via PMDA (Pharmaceuticals and Medical Devices Agency)

PMDA is one of the most rigorous regulatory bodies globally; MDSAP audit significantly reduces duplicative burden

Regulatory pathway for digital health devices (SaMD) is well-defined

Femtech Readiness

One of the world's most advanced femtech markets by per-capita spend on menstrual health and reproductive technology

Strong clinical research infrastructure and data quality

⚠️ Cultural norms around women's health are evolving but remain conservative in some categories — market education investment required

ROI & Infrastructure

Population ~124 million; high healthcare spending and premium consumer health culture

High-margin market for validated, evidence-backed products

⚠️ EF English Proficiency Index: #92 out of 116 — significant language barrier; local partner or Japanese-speaking regulatory lead is non-negotiable

GPI 2024: #11 — very high stability

🇰🇷 South Korea

Regulatory Alignment

MFDS (Ministry of Food and Drug Safety) has progressively aligned with FDA and EU MDR frameworks

MDSAP compatibility pathway is expanding; not yet full membership but convergence is directional

Government actively promoting K-healthcare internationally — creating reciprocal openings for foreign market entry

Femtech Readiness

High digital health adoption and smartphone penetration; strong consumer appetite for health tracking and wearables

Growing awareness of women's health, particularly in fertility and menstrual health tech

Active startup ecosystem with increasing women's health focus

ROI & Infrastructure

Population ~52 million; advanced payer structures and tech scaling infrastructure

Government investment in digital health innovation is substantial

⚠️ EF EPI: #50 — business English limited outside Seoul; local presence required

GPI 2024: #46 — stable, with standard geopolitical considerations given peninsula context

🇮🇱 Israel

Regulatory Alignment

Israeli MOH operates with strong alignment to EU MDR and FDA standards — one of the most harmonised non-MDSAP markets globally

CE mark is a recognised reference standard; dual EU/FDA submission strategies are well-established

Deep bilateral ties with both EU and US regulatory bodies

Femtech Readiness

Exceptionally strong clinical research infrastructure; Israel produces a disproportionate number of medtech innovations relative to population

Highly developed VC and medtech ecosystem; femtech companies including HeraMed are globally recognised

High awareness and openness to women's health innovation; destigmatisation is advanced relative to regional peers

ROI & Infrastructure

Population ~10 million — small absolute market, but high income and high health spend per capita

English proficiency high (EF EPI: #51); business environment is highly accessible to European operators

Strong potential as a clinical trial site and R&D partnership hub, regardless of commercial scale

⚠️ GPI 2024: #155 — reflects active conflict situation as of the 2024 index; market entry decisions require live geopolitical risk assessment, not a static one. The underlying regulatory, clinical, and commercial infrastructure remains among the strongest in this cohort

🇦🇪 GCC (UAE & Saudi Arabia)

Regulatory Alignment

Neither is a formal MDSAP member, but UAE and KSA have adopted CE mark and FDA clearance as primary reference pathways for device registration

UAE MOHAP and Saudi SFDA increasingly streamlined; CE mark provides a strong starting point

GCC Standardization Organization (GSO) harmonisation creates some regional regulatory efficiency

Femtech Readiness

Saudi Arabia's Vision 2030 explicitly references women's empowerment and healthcare improvement — femtech is policy-aligned

UAE has the most open and internationally diverse women's health market in the region

Growing investor interest in femtech and digital health across the Gulf; GITEX Health and Arab Health are active deal-making forums

ROI & Infrastructure

UAE: ~89% of resident population is expatriate (UN data) — genuinely diverse patient population and cosmopolitan business environment

English is the functional operating language for business in both markets

Premium private-pay market; reimbursement structures favour high-value, evidence-backed products

⚠️ GPI 2024: UAE #53 (improved 31 places in 2024 — single largest improvement in the index); KSA requires ongoing monitoring

Cultural distance to women's health topics exists in some categories — local partnership and community navigation are important

🇳🇿 New Zealand

Regulatory Alignment

MDSAP full member (Medsafe)

Strong regulatory alignment with Australia (TGA); joint Trans-Tasman regulatory considerations apply

Simple, transparent regulatory environment — among the most accessible globally for device registration

Femtech Readiness

Progressive women's health policy environment; high health literacy and digital engagement

Maori and Pacific women's health is an active policy and research priority — relevant for inclusive femtech design and clinical evidence

English-speaking, low cultural friction across all standard femtech categories

ROI & Infrastructure

Population ~5 million — too small for standalone commercial focus

Best positioned as a clinical trial jurisdiction, regulatory proof-of-concept market, or Australasian stepping stone alongside Australia

GPI 2024: #4 — among the most geopolitically stable countries on earth

High income per capita; public system (Pharmac) for reimbursement is conservative but private market is accessible

What this means for women’s health startups

The eight markets are not interchangeable, and we are not suggesting a company should pursue all of them simultaneously. The practical read is this:

For a femtech company at the EU/US proof-of-concept stage, with limited expansion resources and no existing presence outside Europe, Australia and Canada are the lowest-friction first moves. They are MDSAP members, English-speaking, culturally accessible, and have enough market depth to justify the investment.

Brazil becomes compelling the moment you have a local partner or are prepared to build one. The MDSAP pathway is a structural advantage that is consistently underutilised by European companies, and a population of 215 million — with the highest demographic diversity of any market on this list — is a significant clinical research and commercial prize.

Japan and South Korea are high-reward markets that require deliberate localisation investment. The regulatory frameworks are accessible through MDSAP and MRA alignment; the human infrastructure needs to be built.

Israel and the GCC are specialist considerations — Israel for companies with strong clinical trial and research ambitions, the GCC for companies targeting the premium private-pay women's health segment and building into the Middle East and North Africa corridor.

New Zealand is genuinely valuable as a regulatory and clinical site — less so as a primary commercial target.

The 4th lens…

At Edge Compliance we want to keep serving US and EU market entries (EU as a continent, incl. UK and CH).

What this analysis taught us is where to put our next focus in terms of partnerships, network, learning, advocacy.

In order to avoid spreading ourselves too thinly, we applied some filters to narrow down the list of high potential regions to a smaller selection. The Edge Compliance lens considers:

Cultural accessibility

Market size

Demographic heterogeneity

Geopolitical stability

Criteria for market selection for Edge Compliance. Which are relevant to your business?

This analysis led us to choose the following areas of focus in addition to our existing focus and expertise:

🇧🇷 Brasil

🇦🇺 Australia

🇨🇦 Canada

🇦🇪 UAE

We trust this will help us help YOU with future-proof regulatory strategy and foresight that is ahead of trends.

References

Institute for Economics & Peace GPI 2024

EF English Proficiency Index 2024

UN World Population Prospects 2024

World Bank Ethnic Fractionalization Data

Vestbee Femtech Market Overview (2024)

Dealroom Femtech Report (2024)

Speedinvest Femtech Investment Analysis

Grand View Research India Femtech Market Outlook 2024–2030

MD+DI FemTech Analytics (2024)

Startups Magazine Southeast Asia Femtech Report

The Recursive CEE Femtech Analysis (2025)

Methodology note: This Deep Dive is based on my original LinkedIn post, reflecting my professional experiences and personal perspectives. Claude AI assisted in elaborating the topic into a broader article by integrating personal notes, literature research, fact-checking and deeper insights on the topic. All analysis and regulatory perspectives are my own, and all content has been reviewed by me for accuracy.

Quantum: The Regulatory Frontier That Will Catch Us Off Guard

Quantum computing is revolutionizing medical device development, but regulatory frameworks aren't ready. Companies like Algorithmiq are achieving 100x precision improvements in cancer therapy using quantum-generated synthetic data—yet FDA's 2025 AI/ML guidance doesn't address quantum validation challenges. How do you validate data you can't reproduce classically? Regulatory science needs quantum-aware frameworks now, before quantum-AI medical devices reach the clinic.

Yesterday, I met Sabrina Maniscalco, CEO of Algorithmiq, at the Italian Tech Forum in Zurich. They develop quantum algorithms for life sciences, including applications in cancer therapy. Despite having taken two courses in quantum physics at university and working extensively with AI/ML medical devices, I found myself needing to educate myself from scratch on what quantum computing means for our field.

What I discovered was both inspiring and unsettling: we're standing at the edge of a paradigm shift in medical technology, and regulatory science isn't even looking in that direction yet.

What Is Quantum Computing and Why Does It Matter?

Classical computers operate using bits, each either 0 or 1. Quantum computers use qubits that can exist in multiple states simultaneously through superposition. Qubits can also be entangled, meaning their states are interconnected regardless of distance. This allows quantum computers to process vast possibilities in parallel in ways classical computers simply cannot replicate.

For medtech, this isn't academic curiosity—it's transformative capability. Classical computers struggle to simulate even simple molecules beyond a certain size. A molecule with just 30 atoms has more quantum states than a classical computer can practically track.

Quantum computers can model:

Drug-molecule interactions at atomic precision

Protein folding and three-dimensional structures

Tumor microenvironments at cellular and molecular levels

Personalized treatment responses based on genetic profiles

The AI-Quantum Hybrid Approach

During our conversation, Sabrina explained: "AI is only as good as the data it's trained on. With quantum computing, we can generate vast amounts of physically accurate data and then train AI on it. Imagine the possibilities from simulating the behavior of ALL atoms in our body."

This is Algorithmiq's innovation: combining quantum computing with AI to address one of AI's fundamental limitations—the need for massive training data.

For many biological phenomena, we simply don't have enough experimental data. It's too expensive, too dangerous, or physically impossible to measure. Quantum computers can generate synthetic training datasets that are physically accurate—based on quantum mechanics—but impossible to obtain experimentally.

Sabrina mentioned that quantum computing capabilities are now available on the cloud, with enterprise access in the million-dollar range annually. For specific computational problems, quantum computers can be more efficient than traditional supercomputers.

Algorithmiq has already announced partnerships with Microsoft (December 2024) and Quantum Circuits (February 2025) to accelerate drug discovery.

A Concrete Example: Photodynamic Cancer Therapy

One particularly compelling application demonstrates quantum computing's real-world impact: photodynamic therapy (PDT) for cancer.

PDT uses special molecules called photosensitizers that are activated by light to produce therapeutic effects. The benefits are significant:

No long-term side effects

Less invasive than surgery

Outpatient procedure

Precisely targeted

Can be repeated at the same site (unlike radiation)

5-10 times less costly than other cancer treatments

The challenge lies in designing these photosensitizer molecules. It requires understanding tiny energy gaps between electronic states—differences that dictate how molecules behave when exposed to light. Classical quantum chemistry algorithms struggle to calculate these energy gaps with the necessary accuracy.

Using IQM's Emerald quantum processing unit and Algorithmiq's advanced error mitigation techniques, the team achieved a 100x improvement in precision compared to results from other quantum hardware providers. This work, part of the Wellcome Leap Q4Bio Challenge, is establishing an end-to-end quantum-centric drug discovery pipeline for light-activated anti-cancer drugs.

They're focusing on the BODIPY class of compounds—next-generation photosensitizers. With quantum computing, simulating their energy landscape becomes possible with unprecedented accuracy, paving the way for better-targeted therapies developed faster and more cost-effectively.

This is happening now.

Closing Health Data Gaps

We also discussed possibilities that particularly resonate with my work in femtech: using quantum computing to simulate complex biological systems like women's physiology to close health data gaps that are difficult or impossible to obtain experimentally.

Women's health research has historically been underfunded. Menstrual cycles, pregnancy, menopause—these introduce biological complexity that makes clinical trials more expensive and results harder to interpret. What if quantum simulation could help bridge these gaps by modeling hormonal interactions and reproductive system responses with atomic-level precision?

The Regulatory Challenges Ahead

Here's the uncomfortable truth: none of medtech's regulations or guidances currently contemplate quantum-AI hybrid diagnostics or therapeutics.

Challenge 1: The Validation Paradox

How do you validate quantum-generated data when you can't reproduce it classically?

The FDA's recent draft guidance on AI/ML-enabled device software (January 2025) requires manufacturers to disclose synthetic data provenance, describe algorithms used to generate it, and demonstrate it preserves clinical correlations. These are sensible requirements for classically-generated synthetic data.

But they break down when the "algorithm" is a quantum computer simulating physics that classical systems fundamentally cannot reproduce. How do you verify quantum-generated molecular data "preserves clinical correlations" when there's no classical ground truth? The entire point of quantum computing is simulating phenomena classical computers cannot.

Challenge 2: Black Box Squared

AI is already a "black box"—how do we maintain our ability to explain and reproduce the operating principles when we layer quantum computing on top?

Explainability is already a regulatory challenge. The EU MDR Article 61 and FDA guidance emphasize transparency in clinical decision-making. But AI models, particularly deep learning, are notoriously opaque.

Add quantum computing—inherently probabilistic, extraordinarily sensitive to environmental interference—and we're layering one form of opacity on another. Yet regulatory frameworks require that medical devices be explainable, reproducible, and transparent.

The FDA's three-pillar framework for Software as a Medical Device asks:

Is there a valid clinical association between device output and clinical condition?

Does the software correctly process input data?

Does use of the output achieve the intended purpose?

For quantum-AI systems, how do you analytically validate "correctness" when there's no classical benchmark?

Challenge 3: Cybersecurity and Q-Day

Quantum computers will eventually break current encryption methods—a threat called "Q-Day." This poses serious risks:

Adversaries can collect encrypted medical data today and decrypt it later

Medical devices relying on current cryptographic protocols will be compromised

NIST announced its fifth quantum-safe algorithm in March 2025, but adoption in medical devices has been slow. Medical device manufacturers should implement quantum-resistant encryption immediately.

What Regulatory Frameworks Currently Exist?

The closest we have are two recent FDA guidances:

FDA Guidance on Real-World Evidence (December 2025) emphasizes that data must be relevant and reliable, with a fit-for-purpose approach. This potentially opens a pathway: quantum-generated synthetic data could be acceptable if manufacturers demonstrate it's the most appropriate method for answering specific clinical questions.

FDA Guidance on AI/ML-Enabled Device Software (Draft, January 2025) addresses data management, synthetic data requirements, performance validation—but all assuming classical computational paradigms.

Neither contemplates quantum-generated training data, validation when classical reproduction is impossible, or uncertainty quantification for quantum probabilistic outputs.

The EU AI Act, MDR/IVDR, and ISO standards similarly don't address quantum computing.

Why This Matters Now

Waiting until quantum devices reach the clinic or reach their "ChatGPT moment" means we'll be reactive instead of proactive, again.

We've seen this pattern with AI. By the time ChatGPT brought AI to mainstream awareness, the technology had been developing for decades. Regulators scrambled to catch up.

But AI builds on classical computing principles we already understood. Quantum computing is fundamentally different. The learning curve is steeper, the validation challenges more complex.

If we wait until a quantum-enhanced diagnostic applies for FDA clearance before starting these conversations, we'll be years behind.

So, what needs to happen?

Regulatory agencies may:

Introduce quantum-aware terminology in guidance documents

Establish working groups bringing together quantum scientists, device developers, and regulatory professionals

Develop validation frameworks specifically for quantum-generated synthetic data

Issue guidance on quantum-resistant cybersecurity for medical devices

Industry may:

Engage early with regulators through pre-submission meetings

Document quantum approaches in detail

Build quantum literacy within regulatory and quality teams

Implement post-quantum cryptography now

Thank you to Sabrina Maniscalco for the thought-provoking conversation, and to Camera di Commercio Italiana a Zurigo for creating the space where these insights happen.

References

FDA Software as a Medical Device (SaMD): Clinical Evaluation

FDA guidance: “Use of Real-World Evidence to Support Regulatory Decision-Making for Medical Devices”

FDA guidance: "Software as a Medical Device (SAMD): Clinical Evaluation"

Methodology Note: This article is based on my original LinkedIn post, reflecting my professional experiences and personal perspectives. Claude AI assisted in elaborating the post into a broader article by integrating personal notes, literature research, fact-checking and deeper insights on the topic. All analysis and regulatory perspectives are my own, and all content has been reviewed by me for accuracy.

Beyond the EU-US paradigm

The global medtech regulatory landscape is shifting away from the traditional EU-US duopoly. The UAE now offers approval timelines 30-50% shorter than US and EU markets, while Mexico and Nigeria introduced comprehensive digital health regulations in 2023 and 2025. Canada, Australia, the UK, and Brazil are implementing bold reforms—from the UK's AI Airlock regulatory sandbox to Brazil's platform tracking over 500 registered software medical devices. This analysis explores strategic implications for medtech companies choosing between the Anglosphere, BRIC nations, Middle East markets, and emerging economies for regulatory submissions.

The recent speech delivered by Canada's Prime Minister at the World Economic Forum prompted me to reconsider my approach to regulatory strategy. Without delving into politics, the address highlighted the extent to which the western world has become US-centric and reliant on American frameworks—a reality that extends fully to the medical technology sector.

This led me to reflect on my own professional practice:

Most of my analysis focuses on comparative regulatory matters between the EU and US.

Most of my medtech clients prioritize EU and US market entry first, and that is what I help them achieve.

Most of my knowledge accumulated over 14 years in healthtech has been built on the default EU-US paradigm.

However, I am far from blind to the strong signals of change emerging on a global level.

Major medtech corporations are beginning to pursue UAE market entry first, given that average regulatory approval timelines are 30%-50% shorter than in the US and EU. Many emerging economies maintain low regulatory barriers for standalone Software as a Medical Device (SaMD) in digital health—large markets such as Mexico and Nigeria only introduced such requirements in 2023 and 2025, respectively. Meanwhile, Canada, Australia, and the UK are taking bold steps to boost health innovation, attract technology companies, and facilitate regulatory compliance.

As former Bank of England Governor Mark Carney stated in his remarks:

"In a world of great power rivalry, the countries in between have a choice: to compete with each other for favour or to combine to create a third path with impact."

"The question is not whether to adapt—we must. The question is whether we adapt by simply building higher walls or whether we can do something more ambitious. The former is easy and ruinous; the latter is difficult and necessary."

This brings me to an important question for the medtech regulatory community.

Beyond the US-EU 'old order', which regulatory focus would you find most valuable for future analysis and guidance?

Anglosphere: Canada, South Africa, Australia, New Zealand

"BRIC" + Japan: Brazil, Russia, India, China, and Japan

Middle East: UAE, Saudi Arabia, Israel

Emerging Markets: Africa, ASEAN, Latin America

I invite you to share your perspective in the poll here

Crans-Montana, a compliance perspective

In the wake of the devastating NYE fire in Crans-Montana, this post reflects on the critical role of compliance and individual accountability in preventing national tragedies, reminding us that regulation is only a burden until the moment it becomes our last line of defense.

Regulation is often seen as pain in the neck… until it isn't. A national tragedy takes place in Switzerland on NYE, and we ask ourselves why didn’t this underground bar have compliant emergency exits? Why wasn’t it inspected in more than 5 years? How could a combustible soundproofing material be permitted and line the whole ceiling? How could staff pull off such a deadly stunt (regularly!) with zero awareness about fire risk? Why the heck were the victims-to-be filming instead of fleeing??

And in particular, how could ALL these hazards manifest simultaneously??

I am horrified by the incident in Crans-Montana (news article). It should never have been. It lights up the painful memory of the Grenfell tower fire in 2017, which had shocked me deeply as I was living in London back then.

We all assume and expect to be protected by regulation. We all assume and expect compliant and responsible behaviour of others. The reality is that if things go south, we are on our own to face the consequences. We all have a responsibility to do our bit, whether it’s fire safety or health.

Being alert to risks, and raising the awareness of others too. Informing yourself and doing your best at least, not ignoring. Holding others accountable by asking questions or reporting unsafe practices. Raising your voice to policy-makers if something isn't enough.

I hope my work does a bit on all these things, within the realm of healthtech, of course, not fire regulation.

As a result, Switzerland now banned the use of pyrotechnics in indoor spaces and is investigating not only the bar owners but the municipality, that did not inspect the bar ONCE in 5 years. The sale of any flammable soundproofing materials is also under scrutiny.

Could this bring into 2026 a bigger wave of respect for regulation and compliance? Am I hopelessly wishful?

Today in Switzerland is a national day of mourning for the 40 victims, mostly teenagers. It breaks my heart to think of what’s left of the 116 injured.

I pray for them and for something like this to not be allowed to happen again - by regulators, by business owners, by fellow citizens, by luck (that's a factor too..🍀), by us all doing our little responsible part in society.

(Image rights: https://www.bbc.com/news/articles/c9dvyyjyj18o)

MDR/IVDR proposal for simplication

This post highlights the European Commission's groundbreaking proposal to overhaul and simplify the MDR and IVDR frameworks, promising more proportionate rules for low-risk devices, reduced administrative burdens for SMEs, and a modern, digital-first approach to medtech regulation in the EU.

12 hours ago the European Commission published THE MOST AWAITED AND CRUCIAL DEVELOPMENT IN A DECADE: its proposal for simplification of the MDR and IVDR. 👏

Alert: it is still only a proposal, albeit official, which has been submitted to the European Parliament and the Council, but will need to go through the ordinary legislative procedure to become binding Union law.

From a first diagonal read, what struck my attention:

🎉 More room for Class I devices, incl software (THANK YOU!)

🎉 Simplified interaction with AI Act

🎉 Codified instruments for open dialogue on classification and access to expert panels

🎉 Easier "equivalence" concept including use of synthetic data,

🎉 Lower NB fee structure for SMEs

🎉 Extended reporting timelines and validity of certificates

🎉 Reduced scope of surveillance audits and conformity assessment

🎉 Built-in flexibility for public health emergencies, breakthrough/orphan devices (i.e. life-threatening, rare, untreated diseases), supply-chain disruptions

Interestingly, but unsurprisingly, it proposes additional requirements for cybersecurity conformity and reporting (beyond what qualifies as medically "serious").

I will share more details of how this would impact specifically medical device startups especially in digital health and femtech.

While it is still ONLY A PROPOSAL, it is sign that EU is listening and actively working to "make [the current rules] easier, faster and more effective and further promote competitiveness, innovation and a high-level of patient safety in this key sector"

We're excited to follow the development of the legislative decision-making process and wait eagerly for the change of an era this (or its variants that will result) will bring to the European medtech sector!

What can we learn from… a progressive Notified Body?

Medtech governance in Europe is highly decentralised, with product certifications also being "outsourced" to private entities (i.e. Notified Bodies). This would be complicated enough if classic Notified Bodies didn't also bring their own enormous challenges to the table: lack of availability, lack of new tech competence, lack of transparency and communication.. Companies feel they have no control over their destiny.

So what's Scarlet doing differently as a Notified Body:

1️⃣ Focus on one subject matter (digital devices only) to ensure top and uptodate competence

2️⃣ Fit the conformity assessment process around the applicant and their timelines

3️⃣ Engage transparently and pragmatically about expectations in pre-sub Structured Dialogues

4️⃣ Scale resources flexibly with externals

and, my favourite,

5️⃣ Train their trusted consultants in an independent manner in order to increase the chance of high quality submissions and enable more effective reviews.

Which other NBs do this? None that I'm aware. But please share if you know any good practices you've experienced.

Therefore, I'm particularly enthusiastic to have been part of this special training session last Friday! Not only with a like-minded NB, but among a group of 18 like-minded regulatory experts ❤️

New times and new tech need a new approach - a mantra of Edge Compliance. I hope other and new NBs will take example.

Note: I'm not affiliated but believe the initiative deserves genuine praise and broadcasting.

Thank you Dan Levy and Sandy Wright at Scarlet - also for the photo credit. Stellar job!

Regulation without borders

Starting two new client projects this week, one on food supplements in France and one on in-vitro diagnostics in Germany, both in womens health!

Very few medtech consultants would feel comfortable touching other verticals (even from MDR to IVDR). But my career started like that when, honestly, I didn't have a choice! Now it's what I enjoy the most, and what I built my agency around.

The hard competences boil down to a few common traits, irrespective of sectors, regs and countries:

➡️ Regulatory definition / classification

➡️ Manufacturing requirements

➡️ Claims and label compliance

➡️ Responsible Person / Entity role

➡️ Notification / Submission procedures

➡️ Review interaction

➡️ Launch and Distribution

➡️ Post-market reporting

After all, it's all about health accountability, and humans have really one way of expecting it - the rest is often noise.

Personally, I find it super fun to come across these analogies, transfer learnings from one area to another and even anticipate cross-sector currents. Excited to get going!

Review timelines for FDA 510k clearance

How long does it take from FDA submission to clearance?

Let's look at the recent data.

The 510k database can be exported and analysed. Format is not humanly readable but makes a fun ChatGPT exercise.

Here is the result of me playing with the database from devices cleared last months (Aug and Sep 2025).

❗ The normal distribution appears to peak around 90 days, the legal obligation for FDA to respond to submissions. Around 30% of submissions were cleared within that timeframe.

❗ Nice peak at 30 days - but don't be too wishful! These are expedited reviews, e.g. changes to existing 510ks or based on prior agreements or expected updates.

❗ Less exciting peak around 270 days, i.e. 9 months. Most submissions receive an Additional Information request, which gives manufacturers 180 days to respond and restarts the clock for FDA after that (further 90 days).

Lesson here?

If you're planning a 510k, a realistic estimate for clearance is nothing less than 6 months. This is what applied to 2/3s of the 400+ applications cleared most recently.

Good quality submissions and preliminary discussions with FDA on the fundamental topics can help prevent Additional Information requests and thus increase the chances of receiving clearance within 90 days.

Does your experience confirm this too?

I will dig more into this database in the coming posts with more insights.

US Gov shutdown: impact on FDA operations

After Republican and Democratic politicians could not agree to pass a bill funding government services, on 1st October the US federal government has shut down. Though not unusual (almost every administration had at least one, lasting from a couple of days to a top 35 days), they create immediate uncertainty for largely Congress-funded agencies such as the FDA.

FDA announced that, based on its contingency plan, it will limit its ops to “mission critical activities including responding to public health emergencies, supporting high-risk food and medical product recalls, and conducting essential surveillance of medical devices and other medical products”.

So in practice, until the end of the shutdown:

🔴 No new submissions accepted (510k, DeNovo) nor payments thereof,

🟡 Ongoing reviews will continue but may suffer delays beyond the mandatory timeframes and potential unresponsiveness,

🔴 Annual fees will not be processed (MDUFA user registration), though due in October for Fiscal Year 2026 - see my previous post on increased fees,

🟢 Medical device recalls and safety surveillance will continue,

🟡 Inspections largely on hold except if “for cause”.

Tough news if you are on the brink of submitting or awaiting a decision. But history tells us these don't last long, so be ready to move fast once the shutdown lifts.

Is it cake? New bordeline guideline rundown

Here the regulatory version of “IS IT CAKE??” 🍰 - if you know the show! Featuring the European Commission’s updated guidance on borderline products published this month.

As someone whose specialty is borderline products and who loves RA developments on the edge, I spent hours digesting its 24 examples of what is or isn’t a medical device - as opposed to drugs, cosmetics, IVD, personal protective equipment (PPE), biocides,..

Frankly, I found half of the examples straightforward, and the other half.. I either struggle to understand the reasoning, disagree or find it inconsistent. Here the main reasons:

INTENDED USE vs MODE OF ACTION, WHO WINS?

MDR defines and classifies medical devices based on the former, while this guidance mostly hedges on the latter. When conflicts arise, this guidance gives priority to the mode of action. There are two, in my opinion, conflicting examples with devices that claim prevention of disease: an STI prevention app and medical examination table covers (i.e. paper roll). The first is not MD, despite processing medical records, using algorithms to assess risk, alerting peers regarding their potential for infection - because “no action on data other than communication”. The second is MD, regardless of its make - because “acts as a mechanical barrier”.

ANYTHING BUT Class I, EVER..

The myth of Class I devices continues. Only one example from here comes out as Class I MD: a rescue bag for patient transport - because "aims to support and protect, [..] avoids worsening of health". Arguably, PPE and Product for Emergency Rescue regulations could be sufficient, so what does Class I MD status really add here? On the other hand, why couldn’t some other low risk examples be Class I (e.g. STI app above, medical calculator for recurrent math)?

It's a continuous learning process for all, and access to practical guidance of this type is very helpful for the health sector as a whole - actually something that FDA does way better (writing style and formal consistency in this manual is quite disappointing).

If we held a geeky RA pub quiz on these examples, how would RA professionals, national authorities and notified bodies score? That would be interesting.

At Swiss Medtech 2025

Swiss Medtech events never disappoint!

Key learnings from attending yesterdays session in sunny Bern (inside a stunning casino!):

1️⃣ US tariffs and lower FDA capacity are discouraging EU/CH startups from going US-first, but there are clever best-practices to work around them.

2️⃣ EU's gap between numbers in MDR applications and certifications is widening in unsustainable ways due to a poor EU-wide governance model for medtech, and how this needs fixing ASAP.

3️⃣ Switzerland is working out creative legal basis to be an attractive alternative (e.g. to fast-track FDA medical devices and to modernise its regulatory framework faster than the EU can)

4️⃣ Emerging markets (e.g. Saudi Arabia) get devices to market 6 months faster than traditional markets, meaning their patients get better outcomes, HCPs get better education, and the healthcare system innovates exponentially faster.

Grateful to Bernhard Bichsel and Sandra Item from ISS AG, Integrated Scientific Services, Daniel Delfosse, Eva von Mühlenen, LL.M., from Sidley Austin LLP, Glenda C. Marsh from Johnson & Johnson MedTech for putting together such an inspiring and informative afternoon!

EU AI Act deployment

Since August 2nd the EU AI Act is in force. But is it?

In practice: not much today, but the clock has started. If your device includes an AI component or uses AI to support decisions it’s time to take a closer look.

For high-risk systems, including many AI-based medical devices, there’s a 36-month transition to comply, i.e. phased implementation. However, some provisions apply earlier (e.g. banned uses of AI, codes of conduct).

Here’s what I see across medtech:

1. Confusion around scope and classification, e.g. AI as a tool for CSV or as part of the intended use?

2. Assumptions that MDR = AI Act compliance, thus reactive attitude to QMS updates upon NB feedback rather than in a proactive manner

3. Teams don't know how to resource it.

Good thing is that I also see a booming AI-related offering from QARA consultants and training providers which can help if you’re stuck on any of the above points. Cool examples (among many others):

• AI-first QARA frameworks and training e.g. Johner Institut GmbH https://lnkd.in/dBSuFfie,

• AI agents for compliance-checking and even FDA review outcome prediction such as Lexim AI or Acorn Compliance,

• GenAI embedded in eQMS tools such as Formwork from OpenRegulatory or Matrix One

What would help your team implementing the AI Act? Curious to hear your challenges and to help you with the right support.

Steep rise in FDA fees for 2025-2026

Alert 🫰 Steep rise in FDA fees from this October:

+19% Annual establishment registration fee from $9,280 to $11,423 (this is the one you pay every year for keeping the right to place a device on the market)

+7% Application fees, e.g. 510k submission from $24,335 to $26,067 (this is the one-off fee for review of a product submission file)

Bad news for early stage medtech businesses and SMEs, in particular since no "small business discount" nor waivers apply on the establishment fee at first registration.

Note, small businesses may qualify for waiver on the establishment fee (2nd year on) and a reduced application fee (e.g. 510k for $6,517 instead of $26,067, new fees) under the SBD programme. Conditions are based on gross sales and justification of "financial hardship", rather than on company size. Worth looking into.

See latest MDUFA fees on the FDA website at this link.

Quality whistleblower - hero vs martyr

How do you make yourself heard when you MUST raise the redflag over design quality, production compliance, clinical safety?

It's an incredibly difficult position to be in, whether you're acting from inside a company or as an external reviewer, stakes are high and office politics (if not even higher politics), budget concerns, along with own self-limiting beliefs, come into play giving you many reasons why you shouldn't follow your gut. Maybe I'm wrong, maybe it's all well. Or maybe it isn't?

I've been in this position before a couple of times as PRRC. It's dire, sleepless nights, conflict escalation. Escalate it to whom? If the technicians or QA's voice is not heard, and your voice as PRRC is not heard, then you hope external parties such as lawyers, consultants, CROs, reviewers will be more effective gate keepers, but then they aren't. They may overlook things or also have their own interests at play. Then who is left to protect the patient? Who is going to stand up and stop the chain of events before it's too late?

The story of Frances Oldham Kelsey, FDA medical reviewer in the 60s who refused to approve Thalidomide is a great example, and similarities can be seen in other preventable disasters such as Titan's OceanGate, Boeing's 737max MCAS software, or Chernobyl to name the most famous. All had a long chain of brave flag raisers in a culture that shut them down..

Culture is key and of utmost importance in medtech. Accountability, feedback and psychological safety create space for risks to be raised and taken seriously at any stage of a project. So called "Type 1 decisions" in business, i.e. non-reversable (launch or not launch?) need true raw information, not just the glossed version that the manager is willing to lend an ear to.

A culture that integrates Quality as their biggest asset and strategic partner will value anyone who raises issues, mistakes, inefficiencies, with a view of preventing not only harm but also resources and reputational risks.

I'm so deeply passionate about driving such cultural shifts and help teams innovate in the most progressive, forward-looking and responsible ways.